Prohibition of Acceptance of Deposits by Unincorporated Bodies

|

Prohibition of Acceptance of Deposits by Unincorporated Bodies

(Governed by S. 45S of the Reserve Bank of India Act, 1934)

| 1. Who can borrow |

Circumstances |

From whom? |

| Individual & Firm |

1. a) If his/its business wholly/partly includes any activities specifiedin S. 45I(c) OR b) If his/its principal business is receiving deposits under any scheme/arrangement/manner or lending in any manner.

|

Only from his relatives or relatives of any partner but not from partner(s). |

| |

2. In any other case. |

Any person. |

| Unincorporated association of individuals |

1. If engaged in business specified above. |

No one. |

| |

2. In any other case. |

Any person. |

The position applicable from 01.04.1997 is as follows:

2. Deposit is defined to include any receipt of money by way of deposit or loan or in any other form, but excludes amounts :

| Received as way of |

Received from |

Received by |

| a) Share Capital |

a) Any banking co. including Scheduled/ Co-operative Bank

|

Subscription to a client’s fund |

| b) Partners Capital |

b) IDBI/SFC/Specified financial institution under IDBI Act/RBI Act |

|

| c) Security/Earnest Money/Advance against

orders |

c) Individual/firm/AOP not being a body corporate registered under any money lending enactment |

|

| d) Credits in the account on Sale of property |

|

|

3. Deposits held as on 1.4.1997 not in accordance with (1) above, shall be repaid immediately when due or within 3 years from 1.4.1997 whichever is earlier. RBI, on application may extend this period by not more than 1 year, specifying any conditions.

4. On and from 1.4.1997, no person referred to in (1) shall issue or cause to be issued any advertisement in any form for soliciting deposit.

5. Activities contained in S. 45I(c) are Financing (Loans etc.); Investment (Shares, debentures, etc.); Hire Purchase; Insurance, Chit-fund or Kuries; Collecting and disbursing moneys in any manner under any scheme/arrangement.

But does not include if principal business is that of agricultural operations, industrial activities, purchase/sale of goods (not securities) or providing services, purchase, construction/sale of immovable property.

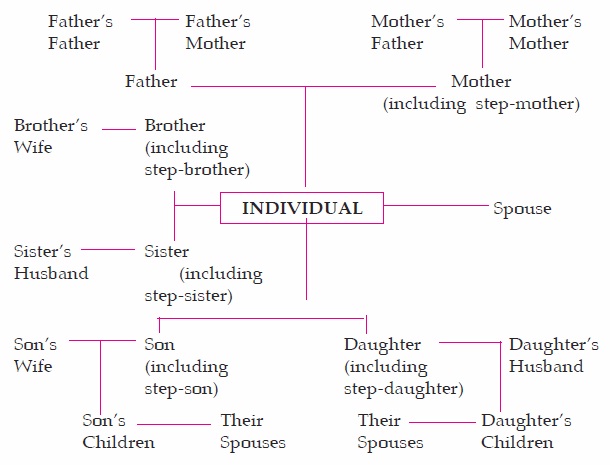

6. For the above purpose, a person shall be deemed to be a relative of another, if they are :

- Members of an HUF;

- Husband and wife;

- Related in the manner indicated in section 6(c) of the Companies Act, 1956 as under :

Back to Top

|