Minimum Alternate Tax (MAT) and Alternate Minimum Tax (AMT)

|

Minimum Alternate Tax (MAT)

1. In the case of companies, if tax payable on its total income as computed under the I.T. Act, 1961 in respect of any previous years, is less than 18.5% of its “book profit”, then such book profit shall be deemed to be the total income of the company and tax shall be payable at 18.5% on such total income.

The profit and loss account should be prepared in accordance with Parts II and III of Schedule VI of the Companies Act, 1956.

The Accounting Policies, the Accounting Standards adopted for preparing such accounts and the method and rates adopted for calculating the depreciation, shall be the same as have been adopted for the purpose of preparing such accounts and laid before the company at its AGM.

From Assessment Year 2013-14 onwards, section 115JB will be applicable even to companies that are not required under section 211 of the Companies Act, 1956 to prepare their profit and loss account in accordance with Schedule VI of the Companies Act, 1956. The profit and loss account prepared in accordance with Regulatory Act governing such companies, would be taken as basis for computing book profit under section 115JB.

2. “Book Profit” means the net profit as shown in the profit and loss account, as increased by –

- The amount of income-tax paid or payable, and the provision therefor; or

- The amounts carried to any reserves, by whatever

name called other than a reserve specified under section 33AC; or

- The amount or amounts set aside to provisions

made for meeting liabilities, other than ascertained liabilities; or

- The amount by way of provision for losses of subsidiary companies; or

- The amount or amounts of dividends paid or proposed; or

- The amount or amounts of expenditure relatable to any income to which section 10 [other than the provisions contained in section 10(38) or section 10A or section 10B or section 11 or section 12 apply];

- The amount or amounts of expenditure relatable to income, being share of assessee in the income of an association of persons or body of individuals, on which no income tax is payable as accordance with the provisions of section 86;

- The amount or amounts of expenditure relatable to capital gains arising on transactions in securities (other than short term capital gains arising on transactions on which securities transaction tax is not chargeable) accruing or arising to

Foreign Institutional Investor which has invested in securities in accordance with SEBI Regulations;

- The amount representing notional loss on transfer of shares or a special purpose vehicle to a business trust in exchange of units allotted by that trust etc.

- The amount of depreciation;

- The amount of deferred tax and provision therefor;

- The amount or amounts set aside as provision for diminution in the value of any asset (w.r.e.f. Assessment Year 2001-02);

- The amount standing in revaluation reserve relating to revalued asset on the retirement or disposal of such asset, (w.e.f. Assessment Year 2013-14);

- The amount of expenditure relatable to income by way of royalty in respect of patent (developed and registered in India)

If any amount referred to in clauses (a) to (i) is debited to the profit and loss account or if any amount referred to in clause (j) is not credited to the profit and loss account, and as reduced by –

- The amount withdrawn from any reserve or provision, if any such amount is credited to the profit and loss account subject to the proviso stated in the section; or

- Incomes exempt under any of the provisions of section 10 [other than the provisions contained in section 10(38)] or section 10A or 10B or section 11 or section 12 apply, if any such income is credited to the profit and loss account; or

- The amount of depreciation debited to profit and loss account (excluding the depreciation on account of revaluation of assets); or

- The amount withdrawn from revaluation reserve and credited to profit and loss account, to the extent it does not exceed the amount of depreciation on account of revaluation of assets referred to in clause (iia); or

- The amount of income, being share of assessee in the income of an association of persons or body of individuals, on which no income tax is payable in accordance with the provisions of section 86, if any such amount is credited to profit and loss account; or

- Amount of income accruing or arising to a foreign company from

- Capital Gains on securities, or

- Interest, royalty or FTS chargeable to tax as per specified rates

- The amount representing

- Notional gains on transfer of shares/SPV to a business trusts

- Notional gains on carrying amount of said units, or

- Gains on transfer of units u/s. 47(xvii)

- The amount of income by way of royalty in respect of patent chargeable to tax under section 115BBF

- The amount of loss brought forward or unabsorbed depreciation, whichever is less as per books of account. However, for the purpose of this clause –

- The loss shall not include depreciation;

- The provisions of this clause shall not apply if the amount of loss brought forward or unabsorbed depreciation is nil.

- Amount of loss on transfer of units u/s. 47(xvii) in certain circumstances;

- The amount of income by way of royalty in respect of patent (developed and registered in India);

- The amount of profits of sick industrial company during the years in which such company has become sick industrial company under the provisions of Sick Industrial Companies (Special Provision) Act, 1985.

- The amount of deferred tax, if any such amount is credited to Profit and Loss Account.

[“Income tax” as referred to in (a) above will include:

- Any tax on distributed profits under section 115-O or on distributed income under section 115R

- Any interest charged under the Act

- Surcharge, if any, levied by the Central Acts from time to time

- Education Cess on income tax, if any, levied by the Central Acts from time to time

- Secondary and Higher Education Cess on income tax, if any, levied by the Central Acts from time to time]

- Provisions shall not affect carried forward of depreciation and losses under the applicable provisions mentioned in sub-section (3) of section 115JB.

- Profits of an Entrepreneur in SEZ or Developer of SEZ liable for MAT from Assessment Year 2012-13.

- Tax paid under section 115JB for A.Y. 2006-07 and any subsequent year would be allowed as a credit from the normal tax payable for any subsequent year in accordance with the provisions contained in section 115JAA for 7 assessment years (up to Assessment Year 2009-10), 10 assessment years from assessment year 2010-11 and fifteen assessment years from AY 2018-19.

- Foreign tax credit in excess of amount of tax credit calculated as per other provisions of Act, shall be ignored while calculation of credit as per MAT

- A report in prescribed form (Form No. 29B, Rule 40B) from an accountant as defined in section 288 shall be furnished along with the return of income.

- In case of conversion of a private company or unlisted public company into Limited Liability Partnership, MATcredit of erstwhile company will not be allowed to the successor Limited Liability Partnership.

- MATProvisions shall not be applicable to and shall be deemed to have been never applicable to a foreign company

- which is a resident of a country with whom India has entered into a Double Taxation Avoidance Agreement or Tax Information Exchange Agreement or the Central Government has adopted any agreement entered into by a specified association and the foreign company does not have any permanent establishment in India; or

- which is a resident of a country with there is no such agreement referred to above, and the foreign company is not required to seek registration under any law for the time being in force relating to the companies.

- From assessment year 2017-18, in respect of a unit located in an International Financial Services Centre which derives its income solely in convertible foreign exchange, MAT will be @ 9% instead of 18.5%

Alternate Minimum Tax (AMT)

Applicability (Sections 115JC, 115JD, 115JEE, 115JF, Rule 40BA, Form No. 29C)

- Limited Liability Partnership claiming deduction under section 10AA, from section 80H to section 80RRB (excluding section 80P) and 35AD* (w.e.f. FY 2011-12).

- Individual, HUF, AOP, BOI Artificial Juridical Person claiming deduction under section 10AA, from section 80H to section 80RRB (excluding section 80P) and 35AD* having adjusted total income (ATI) exceeding ₹20 lakh (w.e.f. FY 2012-13). (deductions u/ss. 80C to 80G are not to be considered).

* Deduction u/s. 35AD (w.e.f. FY 2014-15)

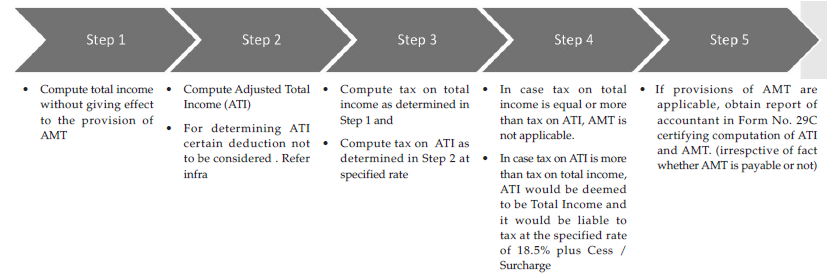

Steps in computing AMT

Computation of Adjusted Total Income (Referred Step 2 Supra)

Limited Liability Partnership, Individual, HUF, AOP, BOI, Artificial Juridical Person

Total income (without considering provision of AMT) as increased by following deductions

- Income based deductions claimed under any section of Chapter VI-A Part C i.e. from section 80H to section 80RRB (excluding section 80P);

- Deduction claimed under section 10AA i.e. units established in Special Economic Zones; and

- Deduction claimed under section 35AD in excess of the amount of depreciation allowable under section 32.

In case of Individual, HUF, AOP, BOI, Artificial Juridical Person, if ATI is below ₹ 20 lakh, AMT is not applicable.

Tax Rate-18.5% + SC + EC+ SHEC (as applicable)

Tax credit

Amount of AMT paid over the normal income tax payable for that year is allowed as tax credit. Such tax credit shall be allowed to be carried forward up to 10 subsequent assessment years.

E.g.

- Tax at normal rate ₹1,00,000;

- AMT ₹9,00,000

- Tax Credit ₹ 8,00,000 [9,00,000 – 1,00,000]

Set off of tax credit

Set off of tax credit is allowed in the assessment year in which normal tax payable by such non-corporate assessee exceeds AMT. Set off of tax credit would be, up to the amount of tax which is in excess of AMT and balance of the tax credit which remains unabsorbed would be allowed to set off in subsequent years. It is provided with effect from the F.Y. 2014-15 that the credit of AMT would be allowed irrespective of the fact whether provisions of AMT is applicable to the assessee in such year or not.

E.g.

- Tax at normal rate ₹10,00,000;

- AMT ₹9,00,000

- AMT Credit available ₹8,00,000

- Set off Tax Credit ₹1,00,000 [10,00,000-9,00,000] Balance credit of ₹7,00,000 can be carried forward for unexpired period.

Foreign tax credit in excess of amount of tax credit calculated as per other provisions of Act, shall be ignored while calculation of credit as per AMT.

Other points

Tax on total income would be reduced by AMT credit for the purpose of calculation of interest u/s. 234A – late filing of return of income, u/s. 234B interest for default in payment of advance tax and u/s. 234C deferment of advance tax. It is specifically provided that all other provisions of the Act shall apply to such non-corporate assessee liable for AMT.

|